Is it permissible to take out a mortgage in Islam?

Are mortgages halal?

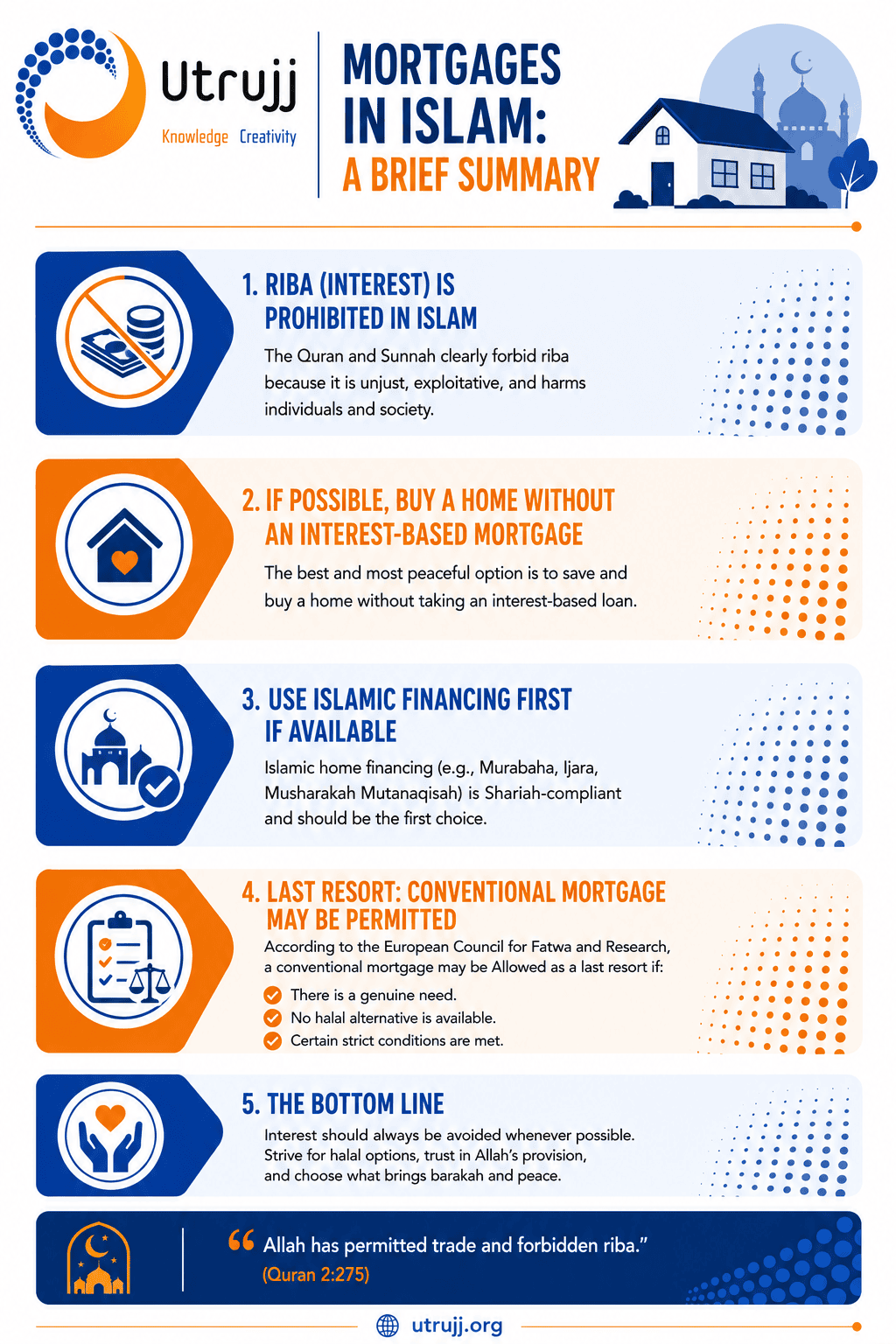

In Islam usury is clearly forbidden. It is a major sin and is one of the seven gravest ones. Those who commit it are considered as waging war against Allah Almighty and His Prophet (peace be on him).

Fiqh Councils throughout the Muslim World state that bank interest is usury.

Those who take ribā (usury or interest) will not stand but as stands the one whom the demon has driven crazy by his touch. That is because they have said: “Sale is but like ribā.’’, while Allah has permitted sale, and prohibited ribā. So, whoever receives an advice from his Lord and desists (from indulging in ribā), then what has passed is allowed for him, and his matter is up to Allah. As for the ones who revert back, those are the people of Fire. There they will remain forever. (2:275)

Allah destroys ribā and nourishes charities, and Allah does not like any sinful disbeliever. (2:276)

Surely those who believe and do good deeds, and establish Salāh (prayer) and pay Zakāh will have their reward with their Lord, and there is no fear for them, nor shall they grieve. (2:277)

O you who believe, fear Allah and give up what still remains of ribā, if you are believers.(2:278)

But if you do not (give it up), then listen to the declaration of war from Allah and His Messenger. However, If you repent, yours is your principal. Neither wrong, nor be wronged. (2:279)

If you can buy outright

If you can afford to buy a property outright, you shouldn’t get an interest-based mortgage.

If you cannot afford to buy your home

If you can’t afford to buy a home, you need accommodation. What should you do?

Some people will say don’t get a mortgage, pay rent as this is the halal way and interest-based mortgages are haram and are cursed by Allah Almighty. I disagree with this approach.

Renting is not a good long term option

There are many reasons why renting is not a good long term option. Rented houses do not give you a sense of security, as you may be asked to vacate the property. Buying a house means that you can modify it to accommodate your social and religious needs. It removes financial pressure, and once you have bought your house, you are more likely to have financial stability to play a positive role in the community and within the ummah.

The European Council for Fatwa and Research issued a lengthy fatwa in 1999 on the permissibility of mortgages, which is about 12 pages long. In a nutshell, they said that if you cannot afford to buy a house outright, and you are not able to buy it using alternatives – such as taking a non interest bearing loan from family and friends, or Islamic alternatives such as Murabaha (sale at a profit), which is practised by Islamic Banks – then you are permitted to buy a house, by taking an interest bearing mortgage.

The fatwa states that you are permitted to access the haram option of taking an interest bearing loan (conventional mortgage) to buy your home, as long as:

i-The house to be bought must be for the buyer and his household.

ii- The buyer must not have another house.

iii- The buyer must not have any surplus of assets that can help him buy a house by means other than mortgage.

A house can be classified as a need

Accommodation is necessary for individuals as well as families. Allah Almighty has granted His favours upon His servants and showed them His bounties, amongst these is their houses:

“And Allah has made for you in your home an abode” (16:80).

The fatwa is built on the Rule of Darurah i.e. extreme necessity or hajah.

The fatwa is based on two major juristic considerations:

- The agreed upon fiqh rule that extreme necessities make unlawful matters lawful. This rule is derived from five Quranic texts, amongst them:

“He (Allah) has explained to you in detail what is forbidden to you, except under compulsion or necessity”, and

“But whosoever is forced by necessity without wilful disobedience, nor transgressing due limits; (for him) certainly, your Lord is oft-Forgiving, most merciful.”

Hajah (need) is considered very close to darurah (extreme necessity) in Islam. If something is classified as darurah, it allows you to access the haram with limitation and in situations of acute need.

Therefore when we have a need, we are allowed to use something which is otherwise prohibited, as long as we have a valid reason. As Allah stated in the Quran, those who might die unless they consume something haram, are permitted to consume it to protect their life. But beyond that, they are not allowed to indulge in it, or consume it beyond their needs.

Hajah is something which places a Muslim in difficulty, when it is not fulfilled, even if he/she can do without it. Darurah or extreme necessity, on the other hand, is that which the Muslim cannot manage without. Allah Almighty stated in Sura Al-Haj and Al-Ma’idah that He does not want us to be a state of difficulty:

“And He has not laid upon you in religion any hardship” (22:78).

“Allah does not want to place you in difficulty, but He wants to purify you, and to complete His Favour to you that you may be thankful” (5:6).

Explore alternatives before accessing the haram

Before you access the haram, find out if there is an alternative. Explore alternative options first.

As an example, if there is a medication with some alcohol or haram substances in it, the first thing I want to know is if there is a halal alternative. If there is, we do not use the medication with haram ingredients. If there is no alternative, then I say it is permissible. Similarly we do not take the haram option first, which is interest-bearing loans. First try to obtain an Islamic mortgage, if you can afford it. If you can’t afford it, then you may take a conventional mortgage.

If you have an Islamic mortgage and you are struggling with the repayments should you move to a conventional mortgage?

Before jumping to this option, I would recommend you speak to your mortgage lender. Tell them you are struggling and see if they can adjust the payments or spread them differently, or find an alternative arrangement. If this does not work out, and you find that you are getting into more financial difficulties, then switch to the conventional mortgage.

Are Islamic mortgages really Islamic?

Those who say that Islamic mortgages are the same as conventional mortgages but with a different label are ignorant. They do not know the financial structure beneath the financial products. All they see is the similarity. This is what people said in Madinah when they could not see the difference between trade and riba (interest). They asked what the difference was when they both appeared the same, for instance they had deferred sales where they paid 10% more if they paid after 2-3 months. They said this was similar to paying 10% interest on a loan. However, Allah Almighty said they seem similar but in reality they are different. Although they both charged 10%, one is a sale and one is interest. They are not the same.

Allah Almighty said in the Quran:

Those who consume interest cannot stand [on the Day of Resurrection] except as one stands who is being beaten by Satan into insanity. That is because they say, “Trade is [just] like interest.” But Allah has permitted trade and has forbidden interest. So whoever has received an admonition from his Lord and desists may have what is past, and his affair rests with Allah. But whoever returns to [dealing in interest or usury] – those are the companions of the Fire; they will abide eternally therein. (2:275)

In an Islamic mortgage, the Islamic bank buys the house and registers it in their own name; a conventional bank does not buy the house. The bank do not own the house. Next, the Islamic bank leases the house to the mortgagee. The structure is different from a conventional mortgage: depending on if you are a first time buyer or not, there are two types, HPP (hire purchase plan) and Buy to Let. The house is purchased through a diminishing partnership, Musharakah Mutanaqisah, which is not the case in a standard mortgage. In the Islamic mortgage, there are two elements, partnership and lease. Every month you buy shares from the bank. In 20 years, all the deeds are transferred to your name without having to pay a second stamp duty.

The analogy you can use is that of halal chicken it looks the same as non-halal chicken, but one is acceptable to Allah Almighty and the other one is not. They may both be in your dish, but it how they arrived there that makes the difference.

I understand that the market is not as big as the conventional mortgage market, so it is less competitive and therefore it is more costly.

Do you recommend sticking to an Islamic mortgage even though the payments are much higher, as there will be more barakah in your wealth?

I have no doubt of this. The market is more competitive because the overheads are less in the GCC countries. The price is very low compared to conventional, where the capital is big and the market is big. But here the overhead is too much and the market is very limited, so the expenses are borne by the customer. If the bank covers it, it will not be a profitable business. Islamic banks are not charities. They are businesses run on Islamic principles. If someone wants to run his business with Islamic principles it does not mean he runs it as a charity. There are shareholders in the bank and their money has to be protected and they have to have growth in their profit as much as possible.

What is the best way to finance buying a car?

My preference is to avoid interest and if possible buy on cash or take out interest free credit and pay it back before interest becomes chargeable. If you have three months to pay back, don’t pay back in the fourth month.

If you are leasing a car are there hidden interest charges in it?

It depends on the terms and conditions and the small print. Although there is a standard contract across the board, you would have to check the details and then decide. If interest is involved, then don’t take it out.

Higher purchase agreements should be avoided.

If you don’t have enough cash to buy a new car, buy a used car in good condition. Why choose something you can’t afford in the first place? We say in Arabic don’t stretch your leg beyond your rug. Keep your leg within your rug. It means don’t go beyond your means.

Shaykh Haytham Tamim – Culture vs Islam (Western Culture) 2020

Why not listen to all the recordings on the Culture vs Islam course?

Looking for more? Check out: All Utrujj Blogs

Jazakumullahu khayran for spending time learning with us. We need your support to enable us to reach more people and spread authentic knowledge. Every contribution big or small is valuable to our future.

‘If anyone calls others to follow right guidance, his reward will be equivalent to those who follow him (in righteousness) without their reward being diminished in any respect.’ (Muslim)